Why Internal Scores Aren’t Enough: Giving Platforms and Their SMBs More Than a Closed-Loop Credit Score

In 2025, platforms don’t just sell software, they sell money.

Embedded capital products like MCAs (Merchant Cash Advances) have exploded. From Square to Shopify Capital, Toast, Clearco, Bonsai, Parafin, and others, platforms are turning transaction data into capital offers, often faster and more efficiently than banks.

But there’s a risk: these capital programs are built on internal credit models, which don’t travel.

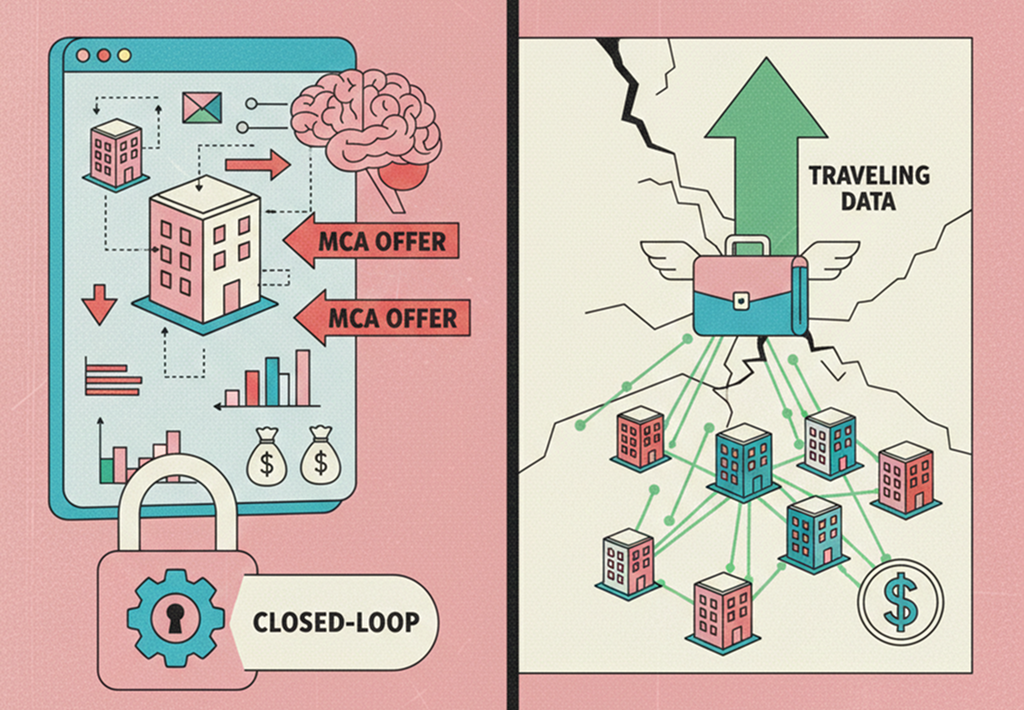

01) Closed-Loop Credit is Booming. But It’s Not Enough.

Merchant platforms today operate inside a closed-loop credit ecosystem.

That means they:

- Use proprietary data to score their users

- Offer funding based on that score

- And in some cases (like Block's Cash App Score), even surface that score directly to customers

It’s efficient. It’s sticky. It’s profitable.

But here's the problem: the rest of the world doesn’t recognize those scores. Not banks. Not equipment lessors. Not landlords. Not vendors.

So as your sellers grow — to 5, 10, 20 locations or $10M+ in GMV — your score becomes a ceiling instead of a launchpad.

02) The Credit Disconnect That’s Hurting Sellers

Most SMBs assume their funding history with your platform is “building credit.” But it's not.

Because many MCA providers, even top-tier ones, don’t report to business credit bureaus, and they often don’t help the business improve its external credit profile.

This disconnect:

- Leads to denials from banks and other lenders, even when sellers are performing well in-platform

- Makes sellers more financially dependent on the platform (which seems like a win… until they churn)

- Reduces access to competitive financing, hurting their ability to grow

03) Why Platforms Need to Care

If you're a capital provider today, you're likely asking: “How do we retain sellers as they grow out of MCAs?”

Here's the answer: help them grow out and up with you.

That means:

- Evolving beyond MCAs to offer term loans, credit cards, and expansion capital

- Giving sellers visibility into external business credit scores

- Helping them actively improve those scores while keeping them engaged in your ecosystem

Because here’s the thing: the fastest-growing sellers will leave if you can't support their financing needs at scale. You're not just fighting banks, you're fighting the next platform that offers a broader credit suite.

04) Business Credit Visibility Is a Strategic Unlock

By offering business credit monitoring, platforms can:

- Help sellers qualify for more capital, from you and other sources

- Improve retention and lifetime value

- Create a bridge to future lending products (term loans, cards, etc.)

Sellers are more likely to borrow (and repay) when they understand what’s helping or hurting them, especially if they can see how your capital product improves their credit profile over time. It all comes down to trust.

Tento Makes It Dead Simple

We built Tento’s Business Credit Monitoring platform to embed directly inside SaaS and marketplace UX.

We offer:

- Real-time access to business credit scores

- Cash flow insights and personalized offers

- Credit-building tips that reward your customers

- Embedded APIs for one-click integration

- A clear path to term lending products, powered by improved credit health

Sellers save time, qualify for more, and grow faster. Platforms get stickier, smarter capital products with better performance and lower CAC.

_Nick_Fancher_Photos_ID6069.jpg)